Carrefour UAE Teardown: SEO Strategy for E-Commerce Website that Turns Visibility into Orders (UAE)

This Carrefour UAE teardown is part of Supramind’s central hub on Ecommerce SEO Services, where we break down how large ecommerce brands can unlock category-level visibility, non-branded traffic, and sustainable organic revenue growth.

Carrefour UAE is one of the cleanest real-world examples of a seo strategy for an ecommerce website in the UAE: massive SKU depth, always-on offers, omni-channel fulfillment (delivery + click-and-collect), and both English + Arabic demand. In my experience, the real question at this scale isn’t “can we rank?”—it’s how visibility compounds into bottom-funnel actions: product discovery → add-to-cart → checkout, plus repeat purchase loops and loyalty/app adoption.

Data note: I’m basing this teardown on the Ahrefs exports and screenshots you shared (overview + top pages + organic keywords + competitors + referring domains). Wherever I estimate conversion impact, I label it clearly as Modeled Example so I’m not implying it’s actual Carrefour internal performance.

Table of Contents

- Introduction

- Executive Summary

- Key Takeaways (At a Glance)

- My Audit Playbook (for UAE eCommerce)

- SEO Snapshot (Ahrefs-style View)

- Competitor Benchmark (High Level)

- The Money Pages That Drive Sales

- Traffic Source Breakdown (Branded vs Non-Branded)

- Traffic by User Intent (Overlapping)

- CTR- & Intent-Aware Projection Model (UAE eCommerce)

- Trust Builders: Referring Domains That Move Rankings

- Backlink Quality & Distribution

- Technical SEO & Localization Wins (eCommerce-specific)

- AI Citations as a New Moat for eCommerce

- Site-Wide Revenue Engine Projection (Organic → Orders)

- Practitioner Key Takeaways (Actionable Notes)

- Final Reflection

- FAQs (eCommerce SEO)

- Disclaimer

Introduction — Why I Analyzed Carrefour UAE’s SEO Engine

Carrefour UAE sits at the intersection of the exact forces that make UAE retail SEO difficult—and profitable:

- High-frequency shopping loops (groceries, household, baby, beauty)

- High-AOV baskets (electronics, appliances)

- Deal-driven demand (“offers”, “best price”, “today delivery”)

- Multi-intent journeys (informational → commercial → transactional)

- Regional behavior (Dubai/Abu Dhabi/Sharjah modifiers + “near me” + Arabic journeys)

When my team audits a retailer like this, we don’t start with “blog topics.” We start with money pages and the conversion path: which pages are pulling demand, what intent they satisfy, and where users drop before checkout.

This teardown stays anchored on three themes I use for UAE enterprise eCommerce work:

- seo strategy for ecommerce website (templates + indexation + internal linking + localization)

- seo for ecommerce product pages (PDP depth, schema, trust, conversion cues)

- backlink strategy for ecommerce (authority that moves competitive PLPs)

Executive Summary

What Carrefour UAE is doing well (data-backed from your exports)

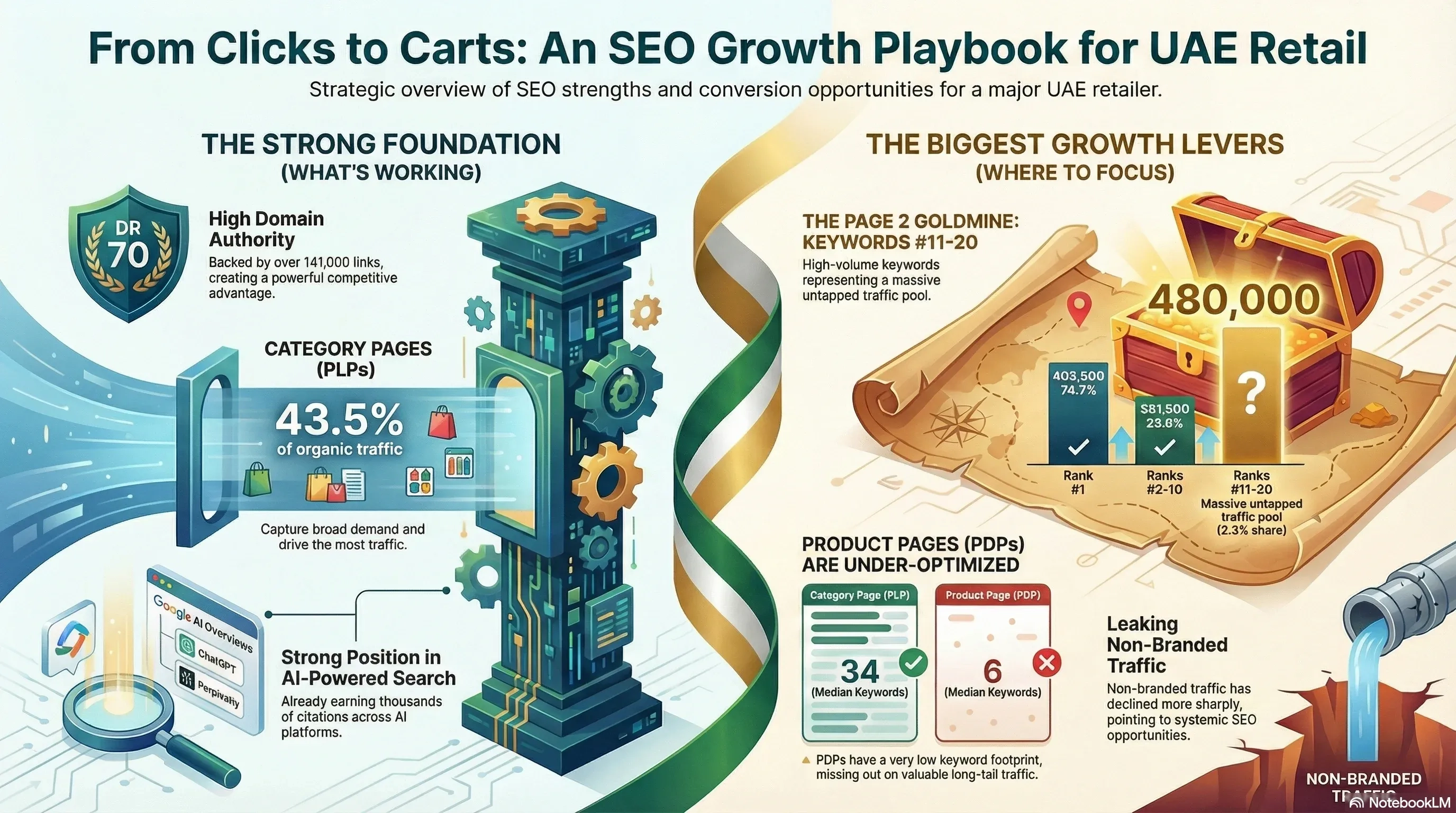

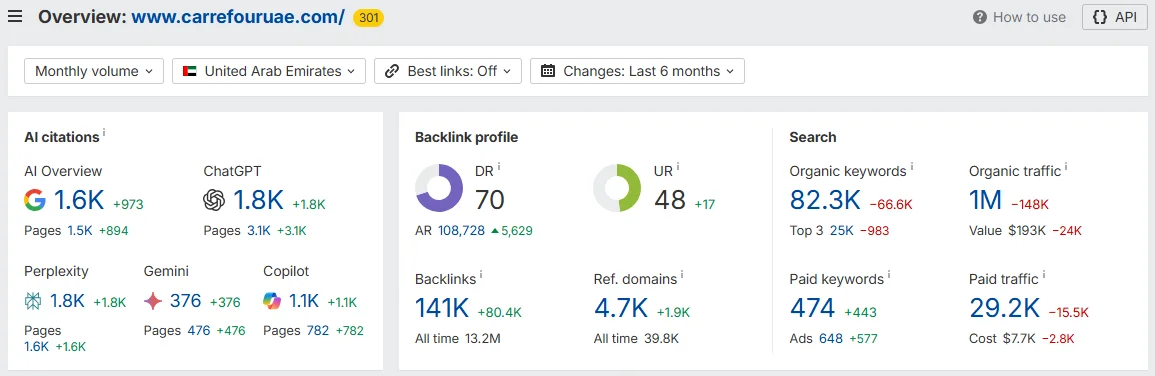

- I’m seeing a strong authority baseline (DR 70) supported by a large link footprint (141K backlinks, 4.7K referring domains).

- In the top pages dataset you provided, PLPs are doing the heavy lifting—that’s exactly what I want to see in a retailer that wants scalable revenue from SEO.

- The offers hub is a legitimate traffic engine and (more importantly) a high-intent landing surface.

- The Ahrefs AI widget you shared shows meaningful AI-citation visibility (ChatGPT/Perplexity/Gemini/Copilot). In my experience, that’s becoming a real moat for product discovery and “best price” behavior.

- Carrefour has indexable store/delivery CLPs—critical for offline uplift and “promise-based” conversion in the UAE.

Biggest opportunities (where I’d focus first if I owned growth/SEO)

- The intent widget shows a bigger drop in non-branded traffic than branded. That usually means the scalable systems (PLPs, indexation rules, internal linking, templates) need tightening.

- High-volume electronics queries are sitting around positions 10–15 in your keyword sample—this is where ROI unlocks fast if you fix hub architecture + PDP depth + links.

- PDPs in the top pages set have a very low median keyword footprint compared to PLPs—this is the clearest signal to upgrade seo for ecommerce product pages.

- Arabic share in the top pages set is meaningful (~16%) but still looks like headroom—especially for grocery and local intent, where Arabic can convert strongly.

- Link distribution is wide, but a large chunk sits in low authority buckets—my team would rebalance toward higher-trust UAE/partner/editorial sources as part of a stronger backlink strategy for ecommerce.

Key Takeaways (At a Glance)

- In my experience, “money pages” (PLPs/PDPs/offers/store locator) are where SEO turns into orders—not generic blog traffic.

- Your dataset shows the biggest upside pool is demand sitting at #11–20: huge volume, low captured clicks.

- A strong seo strategy for ecommerce website in the UAE depends on indexation control + internal linking + scalable templates more than it depends on content volume.

- AI Overviews + ChatGPT-style citations are quickly becoming a discovery layer for retail queries (“best”, “price”, “where to buy”, “offers”).

My Audit Playbook (for UAE eCommerce)

When I audit UAE retail eCommerce, my playbook is consistent because the pitfalls repeat across catalogs:

What I look at (for large catalogs + faceted navigation)

- Demand split: branded vs non-branded, and commercial vs transactional

- Money page coverage: PLPs, PDPs, offers, brand hubs, seasonal hubs, store locator

- SERP reality: Shopping Ads, AI Overviews, Local Packs (CTR is not stable)

- Localization: English vs Arabic parity, Emirates modifiers, “near me” routing

- Trust signals: delivery promise, availability, payment methods, returns, reviews

SERP features Carrefour is competing against (top-keywords sample)

I pay attention to SERP features because they change how much traffic you “deserve” for a given rank. In UAE retail, Shopping Ads and AI Overviews can compress CTR hard.

| SERP feature | #Keywords (top-200 sample) | Share |

|---|---|---|

| Sitelinks | 190 | 95.00% |

| Video preview | 178 | 89.00% |

| People also ask | 157 | 78.50% |

| Thumbnail | 136 | 68.00% |

| AI Overview | 50 | 25.00% |

| Shopping Ads | 48 | 24.00% |

| Local pack | 19 | 9.50% |

| Knowledge panel | 15 | 7.50% |

| Bottom ads | 13 | 6.50% |

| Local teaser | 12 | 6.00% |

| Paid sitelinks | 11 | 5.50% |

| Top ads | 8 | 4.00% |

How I interpret this (UAE retail)

- When Shopping Ads show up (~24% of your sample), I don’t expect classic organic CTR curves. I focus on snippet quality, offer visibility, structured data, and landing relevance.

- When AI Overviews show up (~25%), I treat “citation readiness” like a ranking factor: specs tables, FAQs, comparisons, and clean entity structure.

SEO Snapshot (Ahrefs-style View)

Site snapshot (from your Ahrefs overview screenshot)

| Metric | Current | Δ (last 6 mo) |

|---|---|---|

| Domain Rating (DR) | 70 | |

| URL Rating (UR) | 48 | +17 |

| Ahrefs Rank (AR) | 108728 | +5,629 |

| Backlinks | 141000 | +80.4K |

| Referring domains | 4700 | +1.9K |

| Organic keywords | 82300 | -66.6K |

| Organic traffic (est.) | 1000000 | -148K |

| Paid keywords | 474 | +443 |

| Paid traffic (est.) | 29200 | -15.5K |

When I see a large site losing keywords and traffic over six months, my first suspicion isn’t “Google hates us.” It’s usually one (or more) of these:

- indexation drift (facets/params/duplicates)

- template changes impacting relevance

- competitor category landing expansion

- SERP feature shifts (Shopping Ads / AI Overviews)

- internal linking dilution

Intent split (from your “Organic keywords by intent” widget)

| Bucket | Keywords | Traffic | Δ Keywords | Δ Traffic |

|---|---|---|---|---|

| Branded | 44600 | 604500 | -30.9K | -49.3K |

| Non-branded | 37700 | 442000 | -35.7K | -98.7K |

| Informational | 80300 | 1000000 | -64.4K | -147.2K |

| Navigational | 460 | 40300 | -988 | -1.8K |

| Commercial | 75000 | 965400 | -51K | -145.3K |

| Transactional | 30900 | 330100 | -20K | -64.6K |

| Local | 11700 | 144900 | -19.7K | -14.9K |

| Non-local | 70600 | 901600 | -46.9K | -133K |

What this snapshot suggests (my take)

- Branded demand is still strong (604.5K). That’s a stabilizer during SEO turbulence.

- Non-branded loss is sharper (-98.7K) → the biggest upside is in category architecture + PDP depth + internal linking + indexation discipline.

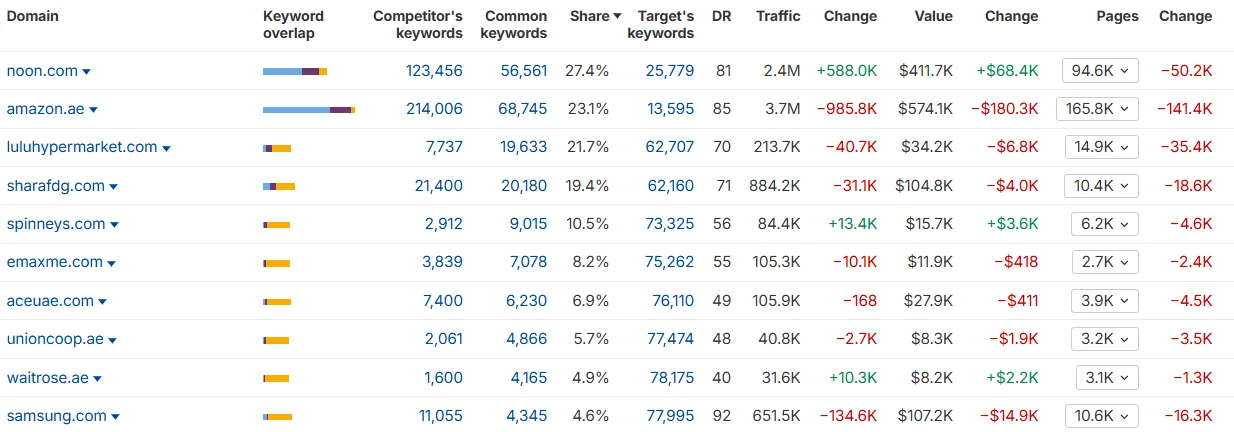

Competitor Benchmark (High Level)

When I plan SEO for UAE retail, I bucket competitors into: marketplaces (Amazon/Noon), category specialists (electronics), and grocery/retail peers. This overlap view confirms Carrefour is fighting on multiple fronts.

| Domain | DR | Traffic | Δ Traffic | No of keywords | Common keywords |

|---|---|---|---|---|---|

| amazon.ae | 85 | 3707954 | -985823 | 214007 | 68744 |

| noon.com | 81 | 2424689 | 587950 | 123456 | 56561 |

| sharafdg.com | 71 | 884245 | -31072 | 21400 | 20180 |

| samsung.com | 92 | 651473 | -134581 | 11055 | 4345 |

| luluhypermarket.com | 70 | 213694 | -40699 | 7737 | 19633 |

| wowdeals.me | 28 | 181839 | -56366 | 10342 | 1597 |

| honor.com | 84 | 172395 | 98664 | 1276 | 448 |

| aceuae.com | 49 | 105907 | -168 | 7400 | 6230 |

| emaxme.com | 55 | 105290 | -10131 | 3839 | 7078 |

| spinneys.com | 56 | 84399 | 13369 | 2912 | 9015 |

| ikea.com | 91 | 72546 | -20256 | 44792 | 11288 |

| carrefouruae.com | 70 | 1000000 | -148000 | 82300 | — |

Where Carrefour wins (conversion advantages)

- Omnichannel trust: physical footprint + delivery reliability typically increases checkout confidence.

- Assortment breadth: Carrefour can win “basket expansion” better than specialists.

- Offers cadence: “offers” as a landing ecosystem is a durable acquisition channel in UAE.

Where competitors can edge ahead

- Marketplaces (Amazon/Noon) dominate breadth + long-tail product pages.

- Electronics specialists can win with category landing depth, comparisons, and link authority.

- Manufacturers steal “price/spec” queries unless Carrefour builds evergreen hubs and stronger entity structure.

The Money Pages That Drive Sales

SEO strategy for ecommerce website starts with money pages (not blogs)

When I look at your top pages export, the story is exactly what I’d expect from a high-scale retailer: PLPs dominate discovery, the homepage captures navigational, and PDPs convert.

| Page type | Pages | Traffic | Avg traffic | Traffic share |

|---|---|---|---|---|

| Category page (PLP) | 138 | 164894 | 1195 | 43.50% |

| Homepage | 2 | 132980 | 66490 | 35.00% |

| Product page (PDP) | 47 | 40599 | 864 | 10.70% |

| Offers / Promotions | 1 | 21545 | 21545 | 5.70% |

| Campaign / landing (CLP) | 7 | 9779 | 1397 | 2.60% |

| Store locator | 2 | 5448 | 2724 | 1.40% |

| Other | 3 | 4198 | 1399 | 1.10% |

What I’d tell a UAE retail leader: If you want fast ROI, you don’t start with “content.” You start with:

- the top PLPs (highest search demand)

- the PDP template (conversion + long-tail rankings)

- the offers ecosystem (high-intent traffic)

- store locator/delivery promise routing (offline + trust)

Language split (top pages set)

| Lang | Pages | Traffic | Traffic share |

|---|---|---|---|

| AR | 51 | 59773 | 15.80% |

| EN | 149 | 319670 | 84.20% |

In my experience, that Arabic share is rarely “maxed out” for retailers. It’s often a signal to build better parity on:

- top grocery categories

- store locator pages

- delivery promise pages

- offers pages in Arabic

Keyword coverage by page type (why PDPs need work)

This is one of the clearest datasets you gave me. It shows how many ranking keywords each page type tends to hold—and PDPs are thin.

| Page type | Pages | Total keywords | Median keywords | Max keywords |

|---|---|---|---|---|

| Category page (PLP) | 138 | 6388 | 34 | 233 |

| Homepage | 2 | 2842 | 1421 | 2459 |

| Campaign / landing (CLP) | 7 | 782 | 99 | 380 |

| Offers / Promotions | 1 | 678 | 678 | 678 |

| Store locator | 2 | 627 | 314 | 541 |

| Other | 3 | 594 | 121 | 381 |

| Product page (PDP) | 47 | 499 | 6 | 55 |

My takeaway: Carrefour’s SEO is PLP-led (good), but the PDP system is under-utilized. This is where seo for ecommerce product pages becomes a direct growth lever:

- higher long-tail capture

- better AI citations (specs/Q&A)

- better conversion (trust blocks)

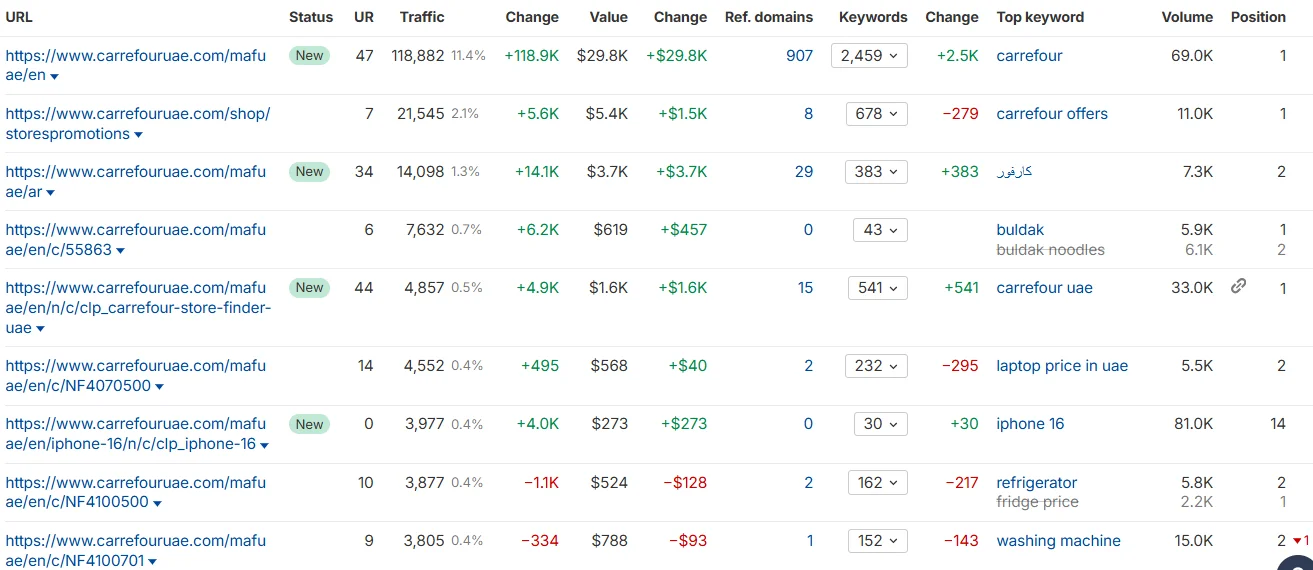

The top 20 “money pages” (what’s actually pulling traffic)

I’m listing these because I want you to see the “why” behind what ranks—most of these are head categories or high-intent navigational/deal pages.

| Page type | Lang | Traffic | KWs | Top KW | Vol | Pos | Path |

|---|---|---|---|---|---|---|---|

| Homepage | EN | 118882 | 2459 | carrefour | 69000 | 1 | /mafuae/en |

| Offers / Promotions | EN | 21545 | 678 | carrefour offers | 11000 | 1 | /shop/storespromotions |

| Homepage | AR | 14098 | 383 | كارفور | 7300 | 2 | /mafuae/ar |

| Category page (PLP) | EN | 7632 | 43 | buldak | 5900 | 1 | /mafuae/en/c/55863 |

| Store locator | EN | 4857 | 541 | carrefour uae | 33000 | 1 | /mafuae/en/n/c/clp_carrefour-store-finder-uae |

| Category page (PLP) | EN | 4552 | 232 | laptop price in uae | 5500 | 2 | /mafuae/en/c/NF4070500 |

| Category page (PLP) | EN | 3877 | 162 | refrigerator | 5800 | 2 | /mafuae/en/c/NF4100500 |

| Category page (PLP) | EN | 3805 | 152 | washing machine | 15000 | 2 | /mafuae/en/c/NF4100701 |

| Category page (PLP) | EN | 3320 | 193 | split ac 1.5 ton | 400 | 1 | /mafuae/en/c/NF4040112 |

| Category page (PLP) | EN | 3281 | 226 | tv 55 inch | 350 | 1 | /mafuae/en/c/NF4050100 |

| Category page (PLP) | EN | 3112 | 204 | vacuum cleaner | 9400 | 1 | /mafuae/en/c/NF4040800 |

| Category page (PLP) | EN | 2933 | 106 | dishwasher | 3100 | 1 | /mafuae/en/c/NF4100800 |

| Product page (PDP) | EN | 2740 | 13 | s25 ultra | 45000 | 11 | /mafuae/en/smartphones/samsung-s25ultra... |

| Campaign / landing (CLP) | EN | 2004 | 21 | carrefour delivery | 350 | 1 | /mafuae/en/n/c/clp_free-delivery |

| Category page (PLP) | EN | 1972 | 125 | water dispenser | 8100 | 1 | /mafuae/en/c/NF4040300 |

| Category page (PLP) | EN | 1913 | 177 | iphone 15 pro max | 43000 | 15 | /mafuae/en/c/smartphones-apple-iphone-15-pro-max |

| Category page (PLP) | EN | 1854 | 139 | air fryer | 8600 | 1 | /mafuae/en/c/NF4050700 |

| Category page (PLP) | EN | 1820 | 153 | water purifier | 5200 | 1 | /mafuae/en/c/NF4040500 |

| Category page (PLP) | AR | 1739 | 37 | ثلاجة | 2500 | 1 | /mafuae/ar/c/9201 |

(Paths shortened for readability.)

What I would do with this list: I’d turn it into a prioritized workplan:

- protect/expand the #1/#2 PLPs (because they’re money printers)

- fix the “stuck” high-volume electronics terms (#10–15)

- upgrade the PDP template (because PDP breadth is currently thin)

Which PLPs dominate (vertical split)

| PLP vertical | Pages | Traffic | Traffic share |

|---|---|---|---|

| Non-food (electronics/home) | 69 | 84525 | 51.30% |

| Arabic category (ID) | 33 | 39478 | 23.90% |

| Food & grocery | 24 | 25677 | 15.60% |

| Marketing / quick commerce | 6 | 7161 | 4.30% |

| Other | 4 | 4728 | 2.90% |

| Marketplace brands | 2 | 3325 | 2.00% |

In my experience, this is also where “conversion modeling” becomes powerful: the same SEO lift on appliances/electronics can be worth 10–20x the AED impact of a grocery term—but grocery drives repeats and LTV.

Top PDP segments (where PDP traffic concentrates)

| Segment | Pages | Traffic | Traffic share |

|---|---|---|---|

| smartphones | 22 | 20683 | 60.10% |

| fish | 2 | 1615 | 4.70% |

| salted-products | 1 | 1265 | 3.70% |

| fridge-351l-to-400l | 1 | 1151 | 3.30% |

| food-colouring-essences | 1 | 1143 | 3.30% |

| probiotic-yoghurt | 1 | 980 | 2.80% |

| sugar-substitute | 1 | 960 | 2.80% |

| full-fat-milk | 1 | 916 | 2.70% |

| capsicum-chilli | 1 | 915 | 2.70% |

| corn-flakes | 1 | 907 | 2.60% |

If I owned the roadmap, I’d use this as justification to:

- rebuild smartphone PDPs as “citation-ready” and “conversion-ready”

- then replicate the template improvements across other high-margin categories

Traffic Source Breakdown (Branded vs Non-Branded)

Sitewide split (from widget):

- Branded traffic: 604.5K

- Non-branded traffic: 442K

- Non-branded drop is sharper (-98.7K) → this is the growth battleground.

In my experience, when a brand like Carrefour is strong, the best incremental SEO wins come from “non-branded category capture,” not from trying to grow branded demand.

Top-keywords sample split (from your keyword export):

- Branded keywords: 34 → traffic 126,069

- Non-branded keywords: 166 → traffic 106,169

That tells me Carrefour is already present for lots of non-branded terms—but the distribution is where the opportunity sits (especially where volume is high and rank is ~10–15).

Traffic by User Intent (Overlapping)

Rank distribution (top-keywords sample)

This table is one of the most actionable in your dataset because it quantifies the “upside pool.”

| Rank bucket | #Keywords | Traffic (top-200 sample) | Total volume (top-200 sample) | Traffic share |

|---|---|---|---|---|

| #1 | 117 | 173400 | 405500 | 74.70% |

| #2–3 | 41 | 33721 | 180400 | 14.50% |

| #4–5 | 17 | 10798 | 153300 | 4.60% |

| #6–10 | 17 | 9025 | 247800 | 3.90% |

| #11–20 | 8 | 5294 | 480000 | 2.30% |

My practitioner takeaway: the #11–20 bucket has 480K volume but only 2.3% of the traffic share in your sample. That’s the exact profile of “high-value uplift” work:

- hub strategy (PLP vs CLP)

- better internal links from parent categories/brands

- stronger PDP content and schema

- better link authority into the cluster

CTR- & Intent-Aware Projection Model (UAE eCommerce)

Modeled Example: Everything below is a modeled example for decision-making. The inputs (keywords/volumes/ranks/URL types) come from your export, but CTR/CVR/AOV assumptions must be validated with analytics.

Opportunity leaderboard (real demand, under-ranked)

| Keyword | Vol | Pos | Traffic | Page | Fix | URL |

|---|---|---|---|---|---|---|

| iphone 16 pro max | 132000 | 14 | 1200 | Product page (PDP) | Strengthen PDP template + link from PLP/brand hubs; add comparison + schema | /mafuae/en/smartphones/apple-iphone-16pmax... |

| iphone 16 | 98000 | 14 | 990 | Campaign / landing (CLP) | Build evergreen PLP/brand hub + redirect/canonical from CLP | /mafuae/en/iphone-16/n/c/clp_iphone-16 |

| samsung s25 ultra | 56000 | 12 | 791 | Product page (PDP) | Strengthen PDP template + link from PLP/brand hubs; add comparison + schema | /mafuae/en/smartphones/samsung-s25ultra... |

| iphone 16 pro | 50000 | 15 | 406 | Campaign / landing (CLP) | Build evergreen PLP/brand hub + redirect/canonical from CLP | /mafuae/en/iphone-16/n/c/clp_iphone-16 |

| s25 ultra | 43000 | 11 | 855 | Product page (PDP) | Strengthen PDP template + link from PLP/brand hubs; add comparison + schema | /mafuae/en/smartphones/samsung-s25ultra... |

| iphone 15 pro max | 43000 | 15 | 344 | Category page (PLP) | Expand PLP copy + curated facets; improve internal links + schema | /mafuae/en/c/smartphones-apple-iphone-15-pro-max |

| pan home | 41000 | 15 | 371 | Category page (PLP) | Expand PLP copy + curated facets; improve internal links + schema | /mafuae/en/c/F1740200 |

| redmi 14c | 28000 | 8 | 983 | Product page (PDP) | Strengthen PDP template + link from PLP/brand hubs; add comparison + schema | /mafuae/en/smartphones/xiaomi-redmi-14c... |

| infinix note 40 pro | 28000 | 7 | 1190 | Product page (PDP) | Strengthen PDP template + link from PLP/brand hubs; add comparison + schema | /mafuae/en/smartphones/infinix-note-40-pro... |

| nintendo switch 2 | 22000 | 10 | 486 | Product page (PDP) | Strengthen PDP template + link from PLP/brand hubs; add comparison + schema | /mafuae/en/nintendo-consoles/nintendo-switch-2... |

| samsung s25 | 20000 | 10 | 490 | Campaign / landing (CLP) | Build evergreen PLP/brand hub + redirect/canonical from CLP | /mafuae/en/samsung-s25/n/c/clp_samsung-s25 |

| iphone 16 pro max price in dubai | 18000 | 10 | 448 | Product page (PDP) | Strengthen PDP template + link from PLP/brand hubs; add comparison + schema | /mafuae/en/smartphones/apple-iphone-16pmax-512gb... |

My direct recommendation: stop relying on short-lived CLPs for evergreen demand. In my experience, the winners build:

- a brand hub (Apple iPhone)

- an evergreen PLP

- PDPs with deep content + comparisons + schema

- internal links that “stack authority” into the cluster

Modeled revenue table (Modeled Example)

| Keyword | Search Volume | Rank | Intent | CTR | Modeled Clicks | CVR | Modeled Orders | AOV (AED) | Modeled Monthly Value (AED) |

|---|---|---|---|---|---|---|---|---|---|

| grocery near me | 17000 | 4 | Transactional | 0.06 | 1020 | 0.022 | 22.4 | 180 | 4032 |

| carrefour offers | 9900 | 1 | Transactional | 0.22 | 2178 | 0.03 | 65.3 | 220 | 14366 |

| buldak | 5600 | 1 | Transactional | 0.22 | 1232 | 0.028 | 34.5 | 35 | 1208 |

| kunafa chocolate | 14000 | 5 | Transactional | 0.045 | 630 | 0.025 | 15.8 | 65 | 1027 |

| air fryer | 13000 | 4 | Commercial | 0.06 | 780 | 0.012 | 9.4 | 350 | 3290 |

| vacuum cleaner | 9200 | 1 | Transactional | 0.22 | 2024 | 0.01 | 20.2 | 450 | 9090 |

| refrigerator | 6400 | 2 | Commercial | 0.13 | 832 | 0.007 | 5.8 | 1700 | 9860 |

| laptop | 14000 | 2 | Commercial | 0.13 | 1820 | 0.006 | 10.9 | 2500 | 27250 |

| iphone 16 pro max | 132000 | 14 | Commercial | 0.011 | 1452 | 0.004 | 5.1 | 4500 | 22950 |

| iphone 16 | 98000 | 14 | Commercial | 0.011 | 1078 | 0.004 | 3.8 | 3800 | 14440 |

| samsung s25 ultra | 56000 | 12 | Commercial | 0.014 | 784 | 0.005 | 3.5 | 4200 | 14700 |

| redmi 14c | 28000 | 8 | Commercial | 0.026 | 728 | 0.008 | 5.8 | 700 | 4060 |

| infinix note 40 pro | 28000 | 7 | Commercial | 0.03 | 840 | 0.008 | 6.7 | 900 | 6030 |

| nintendo switch 2 | 22000 | 10 | Commercial | 0.02 | 440 | 0.005 | 2.2 | 1500 | 3300 |

6.3 Roll-Up Summary (Modeled Example)

- Modeled clicks: 15,838

- Modeled orders: 211.4

- Blended AOV: ~AED 641

- Total modeled monthly value: ~AED 135,603

Rank-Uplift Opportunity (#3 → #1) on high-AOV terms (Modeled Example)

| Keyword | Search Volume | Current rank | Scenario rank | CTR% | Clicks | Orders | Monthly Value (AED) |

|---|---|---|---|---|---|---|---|

| iphone 16 pro max | 132000 | 14 | 14 | 1.1 | 1452 | 5.1 | 22869 |

| iphone 16 pro max | 132000 | 14 | 3 | 9 | 11880 | 41.6 | 187110 |

| iphone 16 pro max | 132000 | 14 | 1 | 22 | 29040 | 101.6 | 457380 |

| iphone 16 | 98000 | 14 | 14 | 1.1 | 1078 | 3.8 | 14337 |

| iphone 16 | 98000 | 14 | 3 | 9 | 8820 | 30.9 | 117306 |

| iphone 16 | 98000 | 14 | 1 | 22 | 21560 | 75.5 | 286748 |

| samsung s25 ultra | 56000 | 12 | 12 | 1.4 | 784 | 3.5 | 14818 |

| samsung s25 ultra | 56000 | 12 | 3 | 9 | 5040 | 22.7 | 95256 |

| samsung s25 ultra | 56000 | 12 | 1 | 22 | 12320 | 55.4 | 232848 |

My core point: leadership ROI shows up fastest when you move a few high-AOV terms from page 2 into the top 3, supported by strong money pages and authority.

Trust Builders: Referring Domains That Move Rankings

In my experience, “more links” doesn’t win in UAE retail—the right ecosystems win. The links that move rankings for competitive PLPs usually come from:

- UAE media and credible local publications

- banks/cards promo partners (cashback pages drive real shoppers)

- brand/manufacturer partners (electronics + appliances in particular)

- mall/community partnerships (especially for store locator + offline intent)

This is why my team builds link plans that point into:

- top category hubs

- offers/promotions

- store locator and delivery promise pages

—not just the homepage.

Backlink Quality & Distribution

Backlink attributes (from your screenshot)

| Backlink attribute | Backlinks | Share |

|---|---|---|

| Followed | 84095 | 59.50% |

| Not followed | 57222 | 40.50% |

| Nofollow | 57215 | 40.50% |

| UGC | 24 | 0.00% |

| Sponsored | 138 | 0.10% |

A ~40% nofollow ratio is not automatically “bad” (brands get lots of cited/no-follow mentions), but it does mean you need enough editorial followed equity pointing to commercial hubs to win category fights.

Backlinks by UR bucket (from your screenshot)

| UR bucket | Backlinks | Share |

|---|---|---|

| 0–9 | 71928 | 50.90% |

| 10–19 | 29490 | 20.90% |

| 20–29 | 7734 | 5.50% |

| 30–39 | 11700 | 8.30% |

| 40–49 | 1609 | 1.10% |

| 50–59 | 14232 | 10.10% |

| 60–69 | 2087 | 1.50% |

| 70–79 | 1680 | 1.20% |

| 80–89 | 395 | 0.30% |

| 90–100 | 462 | 0.30% |

When over half of link volume sits in the lowest authority buckets, my team’s strategy is to raise the ceiling:

- fewer low-quality mentions

- more high-trust editorial/partner links

- direct links into category hubs and evergreen brand pages

That’s the backbone of a practical backlink strategy for ecommerce for UAE retail.

Technical SEO & Localization Wins (eCommerce-specific)

SEO strategy for ecommerce website = indexation control + scalable routing

At Carrefour’s scale, technical SEO isn’t a checklist—it’s a profitability lever. In my experience, the big wins come from:

- Faceted navigation control (so Google crawls what earns money)

- Canonicals + parameter discipline

- Pagination and category hierarchy clarity

- Internal linking that mirrors how people shop in the UAE (category → brand → PDP → offers/bundles)

Localization (UAE reality)

From your keyword export, emirate modifiers show up strongly in branded queries, and many map to the homepage/offers.

AI Citations as a New Moat for eCommerce

Your Ahrefs AI widget shows Carrefour already has real traction here. In my experience, that’s not vanity—AI discovery is increasingly a shopping entry point for “best price”, “which model”, and “where to buy” queries.

Site-Wide Revenue Engine Projection (Organic → Orders)

When I present to eCommerce leadership, I map SEO into a funnel that merchandisers and performance teams recognize:

- Organic visits → PLP views → PDP views → add-to-cart → checkout

- Store locator intent → store visit / pickup conversion

- Repeat loops: weekly offers, staples, household replenishment

Practitioner Key Takeaways (Actionable Notes)

Here’s how I’d prioritize work for ROI in a UAE retail context:

Highest-impact priorities (in order)

- Fix “high volume, stuck at #10–15” clusters (electronics/appliances) with evergreen hubs + internal links.

- Upgrade templates for seo for ecommerce product pages with reviews/Q&A, specs tables, FAQs, and complete Product + Offer schema.

- Indexation & crawl budget: noindex low-value facets, canonicalize filter variants, and index only curated facet landings.

- Internal linking playbook: category hubs → brand hubs → PDP clusters, plus seasonal/offers paths.

- backlink strategy for ecommerce (UAE-first): bank promos, UAE editorial PR, mall/community partnerships, and manufacturer links pointing to commercial hubs.

Final Reflection

What I see in your data is a site with strong fundamentals: authority, omnichannel trust, and category scale. The compounding advantage from here is not “more content.” It’s:

Authority + indexation control + scalable PLP/PDP templates + UAE localization + AI readiness

That’s how Carrefour (or any UAE retail leader) turns SEO into a durable revenue engine.

FAQs (Accordion)

What should be prioritized first in a seo strategy for ecommerce website?

Start with money pages: top PLPs, the PDP template, offers pages, and store/delivery promise pages—then scale internal linking and indexation rules to protect crawl budget and rankings.

What’s the biggest lever for seo for ecommerce product pages at scale?

Template upgrades that increase keyword breadth and conversions at the same time: review snippets, Q&A, structured specs tables, FAQs, and complete Product + Offer schema (price, availability, ratings).

What makes a backlink strategy for ecommerce work in the UAE?

UAE ecosystems: bank promo partnerships, credible .ae editorial, mall/community partnerships, and manufacturer links—pointed into category/offers/store pages (not only the homepage).

How do you handle faceted navigation without index bloat?

Noindex low-value facet combinations, canonicalize filter variants to the parent category, and only index curated facet landing pages that match real demand and have unique intent.

How should Carrefour measure SEO ROI in AED?

Map keyword clusters to landing pages (PLP/PDP), then measure CTR → PDP views → add-to-cart → checkout → AOV (AED), and add repeat cohorts for grocery/household to reflect LTV, not just first purchase.

Disclaimer

This analysis is based on the Ahrefs exports/screenshots you provided. Any CTR/CVR/AOV and AED impact values are Modeled Examples for illustration and should be validated against analytics, merchandising, and margin data.

Related Links and Resources

Teardowns & Case Studies

Amazon India vs Flipkart SEO

A detailed comparative SEO teardown of how two ecommerce giants battle for search visibility in India.

Spinneys UAE SEO Teardown

Analyzing the successful ecommerce search and content strategies that work for Spinneys in the UAE market.

Etsy Non-Branded Search

Learn how Etsy successfully captures high-volume non-branded search traffic across thousands of categories.

Sephora USA SEO Teardown

An expert analysis of Sephora's highly successful US ecommerce SEO and brand search strategy.

Chewy SEO Strategy

Uncovering the organic search strategies and architectural choices that fuel Chewy's massive ecommerce revenue.

Technical SEO for Large Stores

Key technical SEO considerations, crawl budget optimization, and teardowns for enterprise-level ecommerce sites.

Wayfair Category Page Teardown

A deep dive into how Wayfair structures and optimizes its category pages for maximum organic search visibility.

Sephora Product Page Teardown

A focused teardown of Sephora's product page SEO structure, rich snippets, and on-page optimization.

Tools

Ecommerce SEO Score Calculator

Calculate and evaluate the overall technical and on-page SEO strength of your ecommerce store.

Product Page SEO Checker

Audit and optimize your individual ecommerce product pages for better rankings and conversions.

Category Page SEO Auditor

Analyze your category pages to ensure they are properly structured for maximum organic traffic.

Product Schema Validator

Ensure your ecommerce product schema markup is perfectly structured to win rich snippets in search results.

Heading Structure Checker

Verify the hierarchy and SEO effectiveness of the H1, H2, and H3 tags across your ecommerce pages.

- Log in to post comments

INDIA

INDIA